In a somewhat-expected result, the second most voted topic of this blog’s pre-launch poll was about getting from $100,000 to $1,000,000.

Besides being the logical next step on the ladder of wealth, the fact that there isn’t too much of a gap between the first and second-most voted topic allowed me to assume certain things: that the people I have direct relationships with are the types who are already travelling towards $1,000,000 on their own, or are already thinking big enough about the next stage.

This is a promising start.

On this band, the name of the game is leverage.

What would life be like, if I could clone myself?

...was the question popped up in my mind around the third crisis of my life.

Rather than 26 being the ripe time for a quarter-life crisis, the catalyst had been that it was the second time I was forced out of a job, dealing with immigration’s will-I-won’t-Is, for the third time within the span of 5 years.

At that time, I had managed to save 6-months’ worth of emergency fund, as well as dabbling in a few index funds and some stock picking, betting on both black and red on the efficient market hypothesis. It was a time when $100,000 felt like a huge deal.

Unsatisfied with finally earning the market rate, I took over other people’s overtime shifts on the regular — almost as a second fulltime job — because every extra dollar was another weave in my safety net, which had anticipated $5,000—$10,000 sized chunks of immigration fees on the regular. I spent weekends in the office on the fast and free corporate internet, learning about how others have made it, in hopes of finding a way out of this precariousness. A perfect A+ student of the FIRE way by any measure.

Then life throws you a curveball, such as finding out that the company that had been employing you for the past year and a half had fumbled your visa transfer, making your employment for the past 1.5 years... questionable.

The immigration incident, though it had “only” costed me a month off the job and ~$7,000 in lawyer fees, was just the straw that broke the camel’s back, because the events that led up to it was the trifecta of disillusionment with the corporate world: don’t hire, don’t promote, don’t support.

That it roused such a visceral reaction in me that had me asking, “how do I not have to work anymore?”

As such, the cloning-myself question was less of a thought experiment, and more of a conduit for the more useful question: “what is me-like in terms of earning money, but is not me?”

It led me to the most common, and often the only, way the average Australians use leverage to build wealth: (residential) property.

Save $10,000 p.a. off your earned income, and you’ll get to $1,000,000 in 100 years.

Save $50,000 p.a., and you’ll get there in 20 years.

Try as I might, at that time, my best only amounted to a savings of $30,000 p.a. The thought of saving $50,000 p.a. didn’t seem possible, when the corporate budget wouldn’t even allow a $20,000 increase — pretax — to pay for the work of 3+ people.

If there were the two of me, I could save $60,000 p.a. to get to $1,000,000 in ~17 years, live off 4% of it — $40,000/year of passive income — and be done with this nonsense.

Now, if I could remain saving $30,000 p.a., but owning something that earns +$40,000 p.a. — such as a $1M property that yields a net +4% return, hypothetically — and suddenly, one gets to live as she does, and get rich in her sleep.

There’s the siren’s call of every passive investment gurus… and there I was, the willing recipient.

$100,000 — $1,000,000 is where the fun begins

Life in the $100,000 — $1,000,000 band, essentially, is when we have enough to cover the bases, and so the excess can be put to work elsewhere.

The lesser one’s needs are, the sooner one can reach this equilibrium of having enough, where the actual amount of having “enough to spare” can even be a two-to-three months’ savings of $10,000.

Anything that’s not consumed in the moment, can be put to work by buying assets, which have their own temperaments and quirks.

It is not so much that $100,000 is some sort of magical turning point when suddenly one has enough, than it is that at $3,000 — $5,000/month to cover the cost of living at a minimum, $18,000 — $30,000 means another 6 months of highly-probable continued existence, buying some breathing room in case said “stable income” suddenly goes through another episodic restructuring.

With that space, there’s time to think about what one can do with the rest.

As such, the big question in this band is: what do you want to buy?

A $100,000 in the bank, as we’ve seen, affords ~10 months of averaged living cost for 4 people.

A $100,000 in a home affords a dream, with all the terms and conditions that a mortgage brings.

A $1,000,000 in the bank, at the burn rate of $10,000/month, affords ~100 months, or around 8.33 years of life in a no-inflation world.

A $1,000,000 in a home affords a liveable retirement, with all the terms and conditions that a pension brings.

These are some of what $100,000 could afford, when seen from the lens of what things cost.

But what kind of life do they truly buy?

With a spare $1 — $100,000, one can afford publicly traded funds, which are priced anything from $0.01 to $500 per share.

With a spare $1,000,000, one can start affording a standalone commercial property, which pays better than most residential property.

These are some of what $100,000 could afford, when seen from the lens of what things pay.

This answers the unsaid, yet universal, question of someone who starts out with 0 financial knowledge: what can I buy? To which the unspoken answer is, “more money, as a conduit to having more choices”.

What, then, do they truly add to one’s life?

An Average Income for an Average Life, Revisited

Previously we posited an “average” couple, earning “Sydney average” salaries, paying for an “average” mortgage of ~$600,000+, with the rest of their cash flow servicing the life of an idealised atomic family of 4.

While it served as a fine example of what significant obligations in the form of a family and a home loan does to one’s degrees of freedom, it did not tell the whole story, when cash flow is not all there is when it comes to things that we consider worthy to call our assets.

The thing that’s common, whether you had bought a personal or investment property, is that this newfound item on the balance sheet now exposes you to the residential property market’s movements.

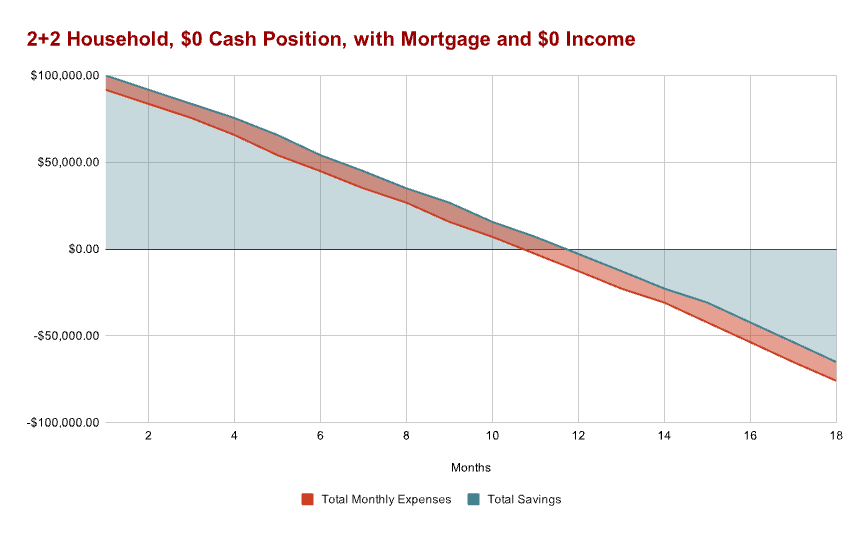

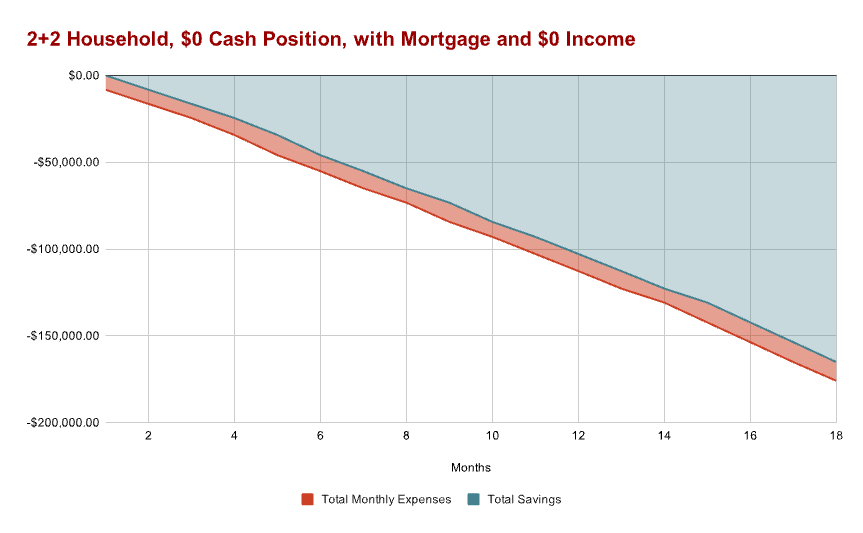

While this chart showed you what might happen in your bank account:

A balance sheet keeps track of what you own, balanced against what you owe, shows you a wider view on what else you can liquidate into cash — if needed.

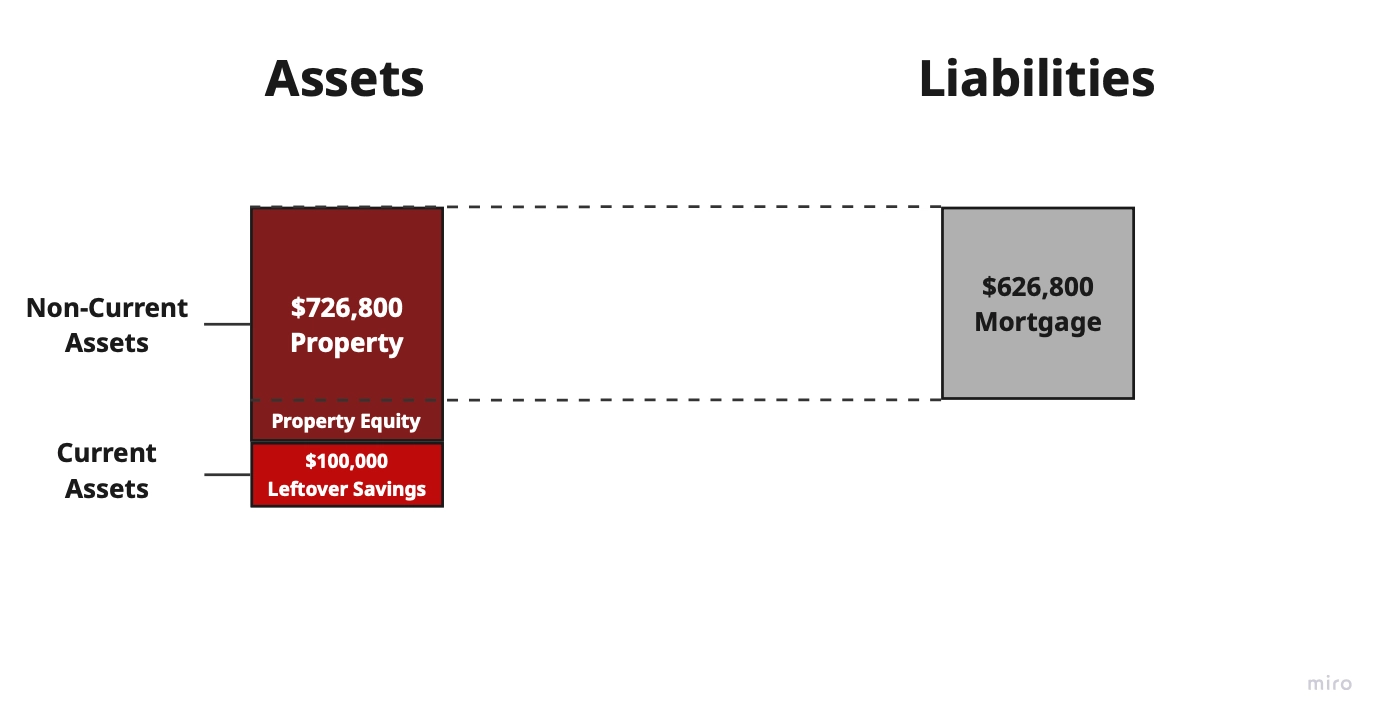

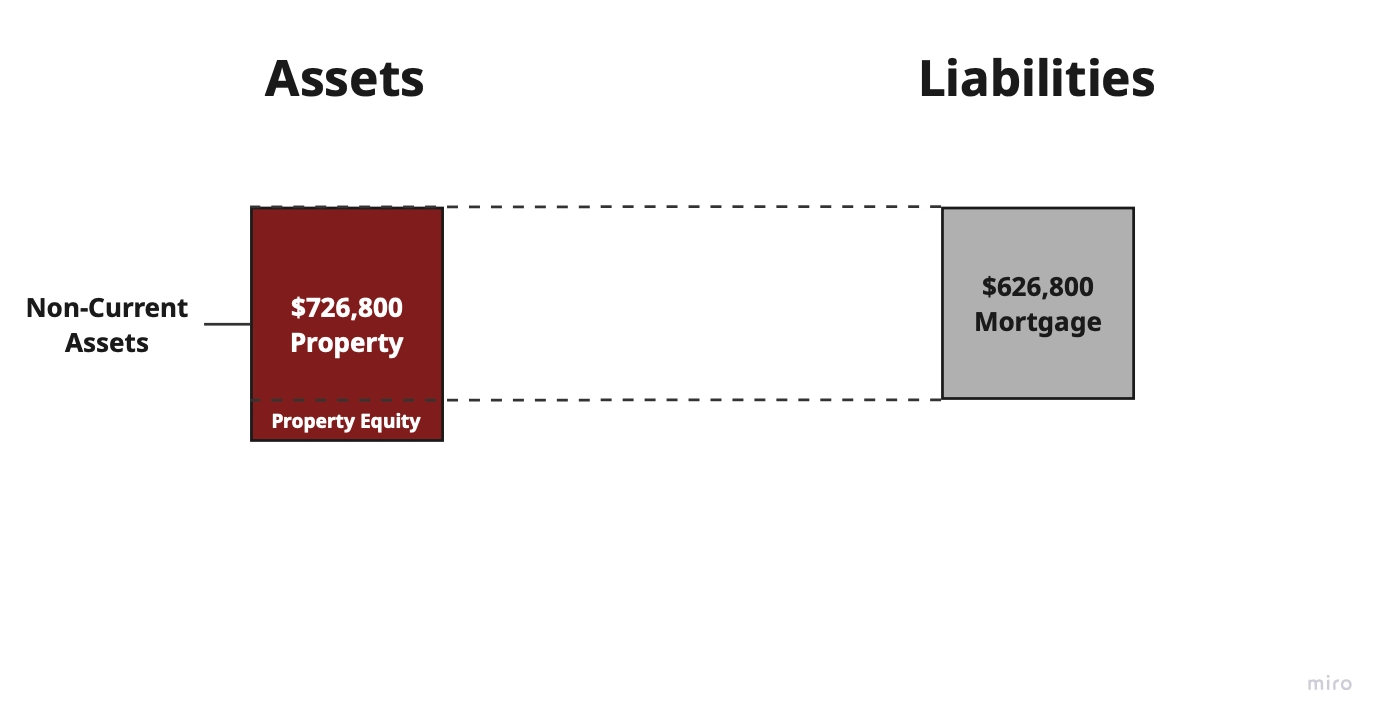

Before buying a house:

After buying a house, with the help of a fairy godmother who covered the down payment:

With some capital and cash, even if the recession scenario eventuates, you do have the choice to liquidate the equity that’s been tied up in the property and get more cash.

As it often pours when it rains, the likely scenario would be that the value of your home decreases along with the job recession, making you lose money if you do sell.

This family has the choice to stay, because they still have that $100,000 in the bank. But is this realistic for most people?

In practice, how many will be able to pull ourselves together to sell at a loss, before they’re forced to?

This is why the family home’s mortgage is priced at -0.20% discount, than an investment property’s.

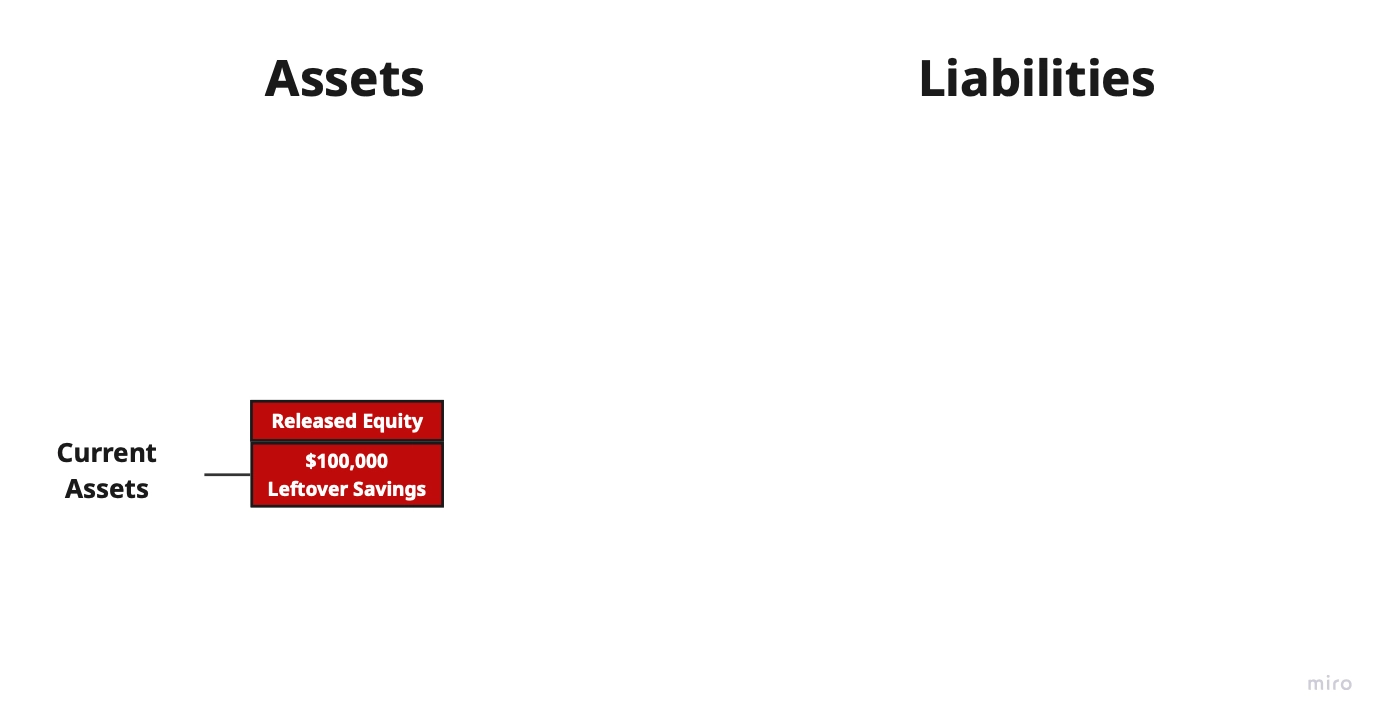

When someone buys a property with their hard-earned savings, this is what usually happens:

The grim reality is that for most people, post-purchase is the moment they’re most vulnerable, as that’s when their repayments is at its highest, and their savings at the lowest, with the penalty of ~1—3 months of illiquidity to convert it back from a home to cash.

The $100,000 of windfall that served as the down payment was an ex-machina that had to be, as the “realistic” scenario of $0 savings post-purchase makes for a terrible example to illustrate how cash burn rate works.

What was meant to be a cautionary tale would’ve turned into a straight-up horror show:

With some good luck, most people can build their savings back up, most of the time. This is the rationale behind the popular advice of “paying down your debt as quickly as possible”: that in comparison to paying the full amount of interest, playing to lose the least by paying the least amount of interest is a very sensible way to reduce one’s risks.

Just as being able to save part of one’s income is the beginning of wealth on the income side of things, paying down debt, too, is a form of saving, when applied on the cost-side part of the equation.

However, building wealth is not about avoiding risks entirely.

With some good luck, you now have a few more possibilities, because cash is not all you have.

Of Cash Flows and Balance Sheets

In the way that light exists as both a wave and a particle, an asset — any asset, really — exists as a duality of cash flow and ownership.

A Tale of Three Brackets: Part 1 talked about cash flow. Specifically, what happens when cash flow dries, as a cautionary tale.

But cash flow is not all there is.

In part 2, which was what some keen readers have asked about, is the part that was purposefully left out: the balance sheet side of the story. It tells the story of ownership, specifically the ownership of things that might make more money for you later.

Arguably cash flow control is the first and the most important financial skill that one could learn, for one can only ever live on money-now; the excess of which can be spent on the things that can bring in money-later.

The more free cash flow one has, that is, the money unspent in the now, the more room there is to move around, paving the way towards the future that eventually becomes the now, which allows us to the choice to do things that doesn’t have to get paid now, if ever, in money. For money only observes those which has a price; such that what isn’t priced in is unobservable, thus worthless within the strict measures of money.

Those which seem counter-productive to others; those which pay a lot more later, those which make one’s life richer beyond the measures of money; these are the things that the immediate money can’t see.

The present eventually became the past, as the rooms created expands into optionality, creating the privilege to choose. Amongst those, primarily, is the choice to say no to the wrong money.

The subset of which that can be measured with money, became line items in your balance sheet. Some add more numbers on your balance sheet, adding to your monetary net worth. Others give you even more cash flow, with which you can buy back time.

All of these, the priceds and the unpriceables, form the life that you now live.

The future, on the other hand, is about time travels and alternate dimensions... which we will explore in another post.

Technically, one does not have to lean on passive investments in order to reach $1,000,000.

Many such persons have “made it” through their inimitable positioning within the inner circles of the future tech unicorns, with many more imitables in the more realistic bands of small-to-midsized exits of $10,000 — $1,000,000.

It just so happened that when one’s ceiling of income at a particular point in time is a fulltime employment, in a context that did not permit a gainful unemployment, on what time can one earn more on?

Thus if the problem is time, the solution would be an income that earns on no time — a “passive” income.

Leverage

The topic of leverage, when touched upon in the context of wealth, unfailingly latches on borrowing money as a leverage to buy assets.

“Buy it with Other People’s Money”, they said sagely. “$0 money down”, so the choir sang. It is, once again, quite insulting, that in the age of unaffordability, that anyone is presumed to be blissfully unaware that buy now pay later is not only for buying Chipotle.

Time, energy, skill, capital are all common ways people leverage to earn more. In the age of attention, that too, is a leverage, as the script that is still writing itself drags us along into the singularity, where attention is all you need.

The common sense that’s not very common is that anything can be an asset, as long as one knows what, where, and how to use it, the way life is long, if one knows how to use it.

“This is the secret to the universe, levers.”

Your Job is Your Asset

When one takes on a student debt to get a degree, one is inefficiently spending to add another leverage — skills and licenses, derivatives of network and social proof really — to one’s market price, with $0 down.

While it’s not impossible to calculate the ROI, the simplest method being the median salary, the inefficiency is twofold: that a 18-year-old who calculates the dollar returns on their degree with all the information on its lifetime valuation is the exception, not the rule, and that the value proposition of a job is not sold on a pure monetary returns on the dollars spent.

Your job is one such asset which is one of the most potent, if only for the fact that with most jobs you can earn money right now, as opposed to most other ventures that ask for a lot of resources upfront — money down to buy the thing, paying for mistakes, paying for ignorance — before one understands the full nature of that particular type of income.

It is never earned from nothing, much to the chagrin of bootstrappers, for where hiring remains a risk to the business, even entry level jobs require some sort of ticket to play: local connections, proof of work, fame-notoriety, or all of the above.

Most publicly listed jobs, the ones that can be found on the job boards, are much like publicly listed companies’ shares: an asset that’s near-100% cash flow, near-0% growth. The idea behind this is the market efficiency: that once something is public, there is enough competing forces in the market to settle to an equilibrium of “fair price”, which is why a job listing is a poor avenue for getting above average returns. It is already, by definition, the price set by the average.

If you choose employment as your main vehicle to wealth, don’t just aspire to qualify for the most jobs on the board; aspire to set your own price.

A job is most people’s first asset. But it doesn’t have to be the only one.

Your Capital is Your Asset

Capital, on its own, is just a measure potential. It is inert until it is used well; in this case, allocated to things that add to one's life, either in more money, thus more potential, or to afford certain kinds of life.

With passive investments, the math is simple, but the execution is… complicated.

Buy $100,000’s worth of investment with cash, and at a 5% p.a. net returns, and it earns you $5,000 p.a.

Buy $1,000,000’s worth of investment with cash, and at a 5% p.a. net returns, and it earns you $50,000 p.a.

While nothing had qualitatively changed, as the investment still only yielded 5% in either scenario, just as one’s hourly rate can remain the same yet one can earn more by trading more time, the more capital is invested the more one can potentially earn.

What if one doesn’t have $100,000 to begin with?

The tyranny of the yield means that turning $5,000 into $100,000 requires seeking the unicorn-level returns of 2000%, but where the unicorns live is in the gated gardens that require a minimum of $100,000 to enter.

If one has but $5,000 on hand, a 100% return on a $5,000 investment would still only yield another $5,000 — before tax. As such, one would be wise to keep working, where a $6,000 nett pay over a $3,000 living costs effectively equates to a net return of 50% every month.

A 50% return every month is very hard to beat. A quality source of income, that comes in without fail every month – with exceptions, is also very hard to beat. This is a very rational view of someone who lives on cash flow alone.

And yet, if there’s an opportunity to earn 14% on “no time”, who in their same rational mind would turn it down?

If one wants to earn more on less and less capital, the game is no longer about size, but rather, quality.

When it comes to capital investments, quality is spoken in percentages and time horizons. Percentages, not only on the returns, but also on the potential loss, the assessment of which is the underrated skill of the quiet compounders.

At what size compared to your total wealth, at what allocation is the risk that you can — and want to — afford?

Are you willing to accept that heads — you’re set for life, tails — it’ll set you back 10-20 years?

Do you go for the 50% returns with the 20% risk of total capital loss, or stick with the 5% government-guaranteed, “risk-free” interest in the bank, and get there in about 20 years?

The blind luck of being born naturally frugal meant that I didn’t have to think in order to save. It meant one less thing to manage; one less noise to the chatter around money. But that’s just about where my luck ran out, for the context I was born into was that of working hard and saving for the unforeseeable, terrifying future.

The second blind luck was that I had never accepted that a bleak future is all there is. And so, I sought ways to make money other than working harder.

In a bid to get to financial security faster than what my below-average salary could afford, I devoured all the free online financial courses I came across — Coursera, edX Harvard courses, Udemy, you name it — in search of the secrets to making money.

A lot of it wasn’t useful. What use was there to be able to model CAPM, when there was only $5,000 to play with? What good would learning macroeconomics have brought, besides magnifying the precarity of one’s situation?

But if one were to become an investor, one must believe in the future where there will be more than $5,000 to allocate.

To fill in the void where the knowledge to make my money work should’ve been, I sought, bought, lost some, gained some more, lived, and finally learned. Less of the ivory-tower, seeking-alpha kind of capital allocation, more of the actually-useful things: what is enough money in the context of one’s life, and where are opportunities to be found?

Resources, when distilled into percentages of dollars and time, then, are the score-kept that allows you to compare opportunities. What gives the best return on the amount of resources given at the shortest amount of time?

When it’s active, the more you can earn on less resources, at a higher certainty and at the least risk of loss, the better.

When it’s passive, the more you can earn on less resources, at a higher certainty and at the least risk of loss, the better.

They are practically identical, because the common sense that’s not very common is that all passive investments were once active endeavours. Instead of time, the fuel of passive investments has been distilled into dollar amounts, which has no worth of its own, until it affords some fractions of materials and other people’s time and energy instead of yours.

Once all of the demands for its resources can be quantified, it requires little to no time to run, at which point it then becomes “passive”.

Those who had forgotten this fact, have lost the plot.

The point of your first capital investment isn’t to make it big. It’s to learn the language. Doing is the only way to convert surface level knowledge into something that’s yours, which is something even LLMs cannot do for you.

Once you get it, you can do it all over again, faster and better this time around.

If the problem is time, the solution would be an income that earns on no time — a “passive” income.

However, passive investments is not without its own problem, none the least being that more money makes more money. Now the problem has shifted from time to size.

The solution?

As it turns out, you can just borrow stuff.

Other People’s Capital are not Your Asset

But they can be borrowed to buy an asset of your own.

Buy $1,000,000 worth of property with 90% debt, and at the same 5% p.a. yield, which now comes in the form of rent instead of dividend, and your property earns you $50,000 p.a. on your $100,000 — before interest costs.

Secure the $900,000 loan at a 4% p.a. interest rate, and $50,000 - ($900,000 * 4%) = $14,000 is what gets paid out every year.

You now earn $14,000 on your $100,000 instead of $5,000, or a 14% ROI. Other people earn that guaranteed 4% yield on their money before the middlemen’s fees, and because it’s their asset, not yours, you have to pay it back at some point.

The money from shares income isn’t green while a rental income’s is blue. On paper, the same mechanism applies everywhere: get cheaper debt than your asset’s returns. Remember the concept of arbitrage 101: buy low, sell high.

Other People, Meanwhile, are Potential Assets

People, when seen in their entirety of a human being instead of piecemeal skills to be bought and capital to bring on, can be great assets that you can never own 100%.

When you buy a $1,000,000 property with 10 other people, this is one subset of it: other people’s capital, otherwise called equity contribution.

While you no longer earn 14% on your $100,000, you have $0 debt in exchange — a big deal depending who you are. As a group, you also are able to buy more expensive assets, which tend to have better returns due to the pricing power effect.

With equity comes voting rights and other non-monetary interests, a situation which at times is called, having “skin in the game”.

Just like any group project experience, when it comes to equity partners, who you bring on matters a lot more than how much they bring in.

With more people there are extra things to manage, in particular their expectations, risk appetite, and life requirements — which always changes — which is why aligning intent in the form of exit opportunities, outcomes, timelines and other things that prevent them from using their capital — is paramount, if there is to be a relationship after the venture.

Most people start out with family and friends as a joint partner, which is easy, but is not always right. Easy, because they are already invested in you in the absence of evidence, but not always right, as family members might not be the professionals you wish they were.

When the working day comprises most of one’s waking hours outside of the home and the family, it is, indeed, better to be alone than in a bad company.

In its most direct upside, only people could introduce you to more opportunities, should one seek audience with generosity. It is for this reason that I should never like to work with misers. Frugal, yes, but never the miserly.

Frugal people give you the best of what they have little of. While they would only order an entree for their lunch, they are somehow never without little treats to give out, or the latest discount hacks to offer.

Misers give you what’s left after they’ve taken what they can, as if candies in glass bowls make for a good Q4.

While what they give out might have been the same nominally, one doesn’t have to be fought tooth and nail in order to give something — anything.

Who is more pleasant to live with?

If one is in want of a good life, one must choose the good problems to deal with.

How to Get Rich Eventually

To make money, earn more, spend less.

There is a ceiling to each source of income, the tipping point where 2x the effort only yields < 50% total returns — that is, in both cash and capital growth combined. The clue is in the quiet voice that says, “it’s not worth it anymore”.

If one’s time can be traded for a lot more per second, as is the case with OpenAI and Anthropic recruits, one doesn’t always have to divert one’s efforts into buying things that can earn on its own time. But those with the salaries that lag behind the cost of living, will often have to.

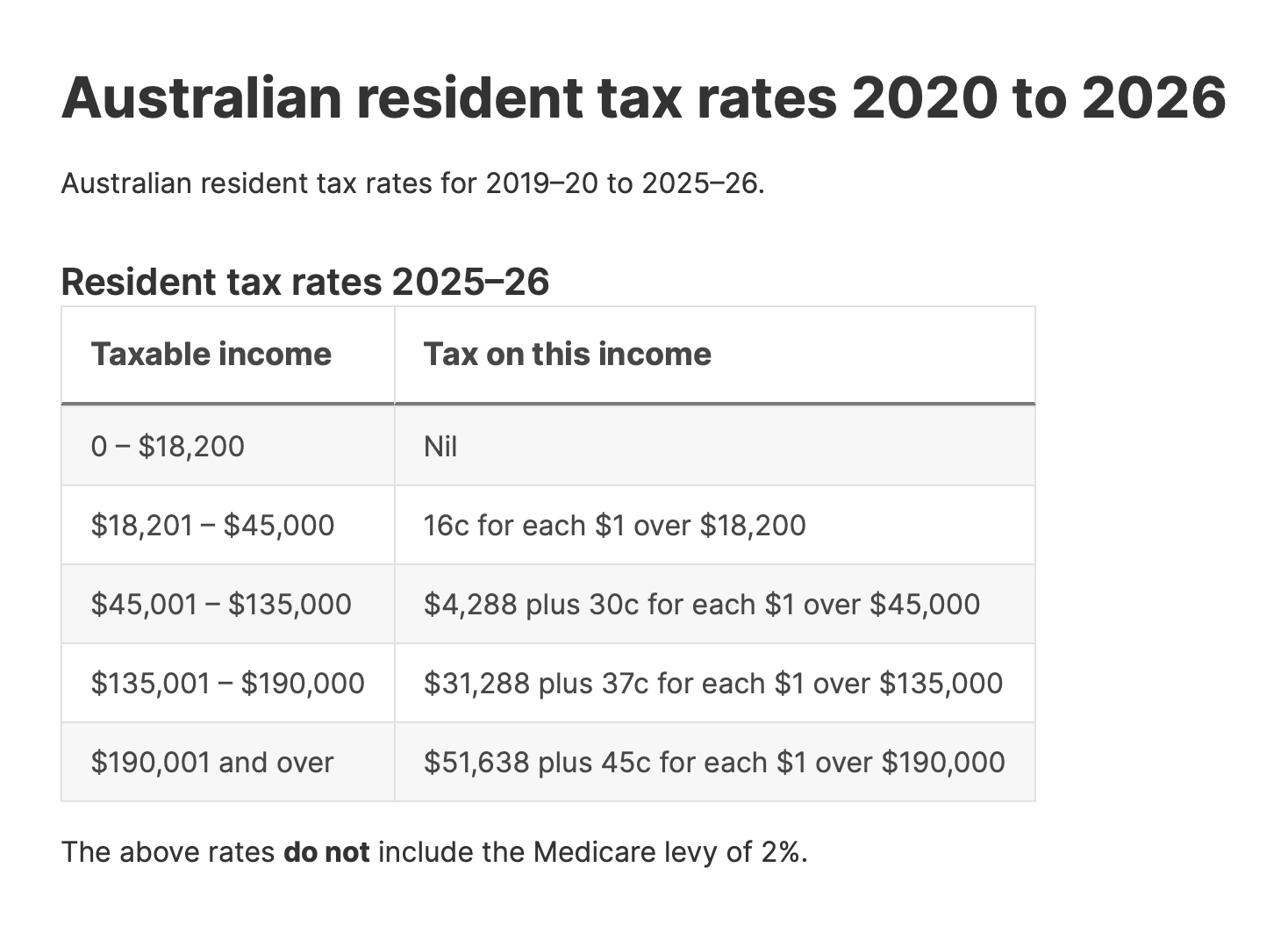

When there’s nothing left to cut out of your personal spending, the next thing one can do is look at how much tax one pays. What income gets taxed less? Where a salary to cover for a minimum cost of living already gets taxed at 30%—45%, though not as good as $0 tax, a 25% maximum tax on capital gains is hard to beat.

The 3-steps to get rich eventually, in a nutshell, becomes:

- earn enough money to start betting on loaded die rolls. 50—90% heads, you win. Tickets start at $0.1 — all the way up to infinity.

- be able to afford the occasional bad luck, so you can recover and try again.

- don’t die and interrupt the compounding unnecessarily.

When one is about to buy an asset, the ideal way is to first decide whether it’s for cash flow or for capital growth, or in other words, if would you like more money now or (hopefully) a lot more money later.

It sounds very sensible in theory, except for one glaring flaw: How would one know what one wants or needs, if one has never tried it herself?

How much can be consumed now, how much is to be sown for the future?

What good is an abundant spring when one cannot survive the winter?

Financial planners can answer this for you based on what works for the average people. That’s their job: to put into perspective what your finances should look like in order to support the average good life. They don’t strive to beat the market, they strive for the 50th percentile.

This is an excellent start, because in the world that lacks universal financial literacy, the average is above average. Not to the extent that one never has to work anymore once it’s achieved, but that life becomes more solveable, because now you have some plans on how to afford the basics.

However… if one wishes of a life of one’s own design, why should one settle for the average?

Of Cash Flows…

Living on cash flow is to live in the now.

It is the one and only present you’ll ever experience, such that the quality of your life is directly related to the quality of your cash flow.

A residential property, for example, is one such asset class that tends to drain cash yet grow in capital, which is why the average experience of homeownership sucks even as one’s net wealth grows. When one can only save $3,612.67 on a very frugal month, $15,000 for the leaking roof or the cracking balcony of an apartment is decidedly unwelcome, even as market forces drive it to gain $50,000 that year.

Getting to $1,000,000, at a monthly personal income of $8,601.67, after a tax of $1,989 and a minimum cost of living of $3,000, equals to a savings rate of $3,612.67, takes 276.80 months — or ~23 years.

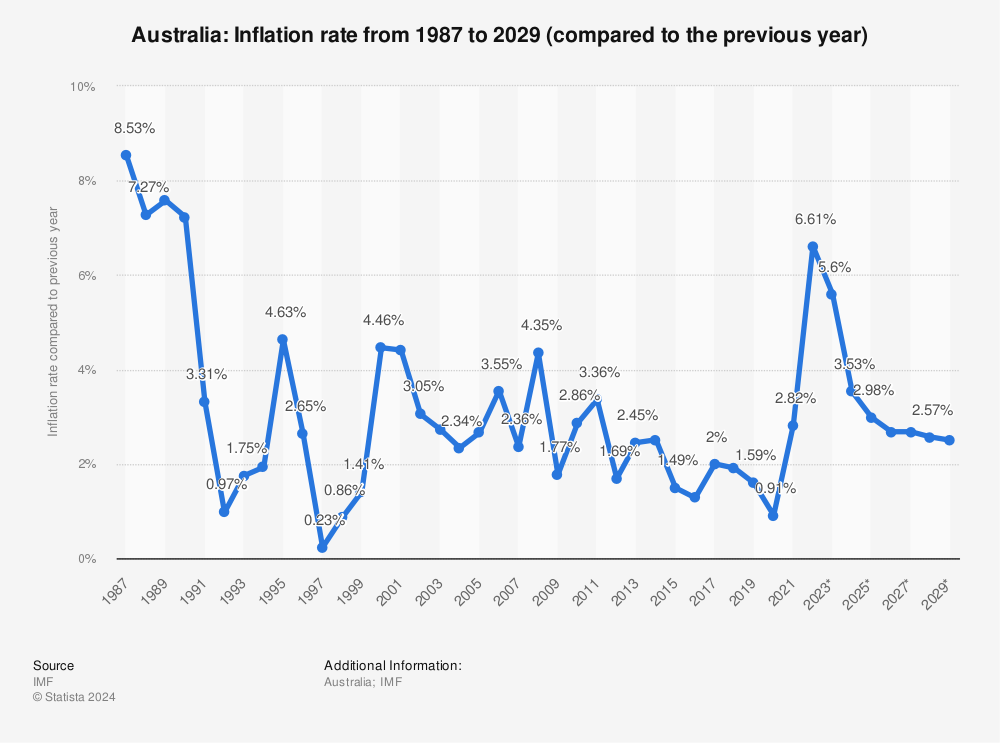

In the face of a wage that hovers around 3% on average…

Find more statistics at Statista

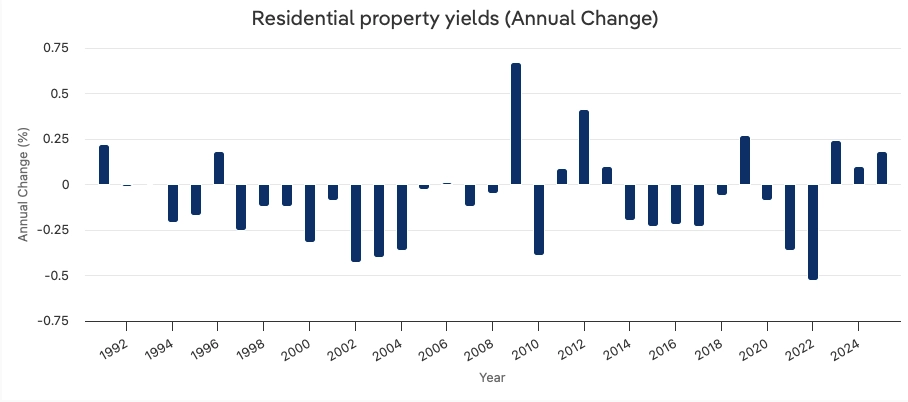

…which attempts to afford the ever-increasing cost of living at around 4%…

Find more statistics at Statista

…we, like most people, implicitly accepts the ceiling to one’s possible income and the floors of one’s expenses, and bargain with the years-to instead.

… and Balance Sheets

Living on capital, on the other hand, is to harvest the potential futures to use in the now.

Where on cash flow, a high-earner earning the extra $222,222 on a 45% tax bracket, or $100,000 after tax, to reach $1,000,000 in 10 years…

With a 90% leverage on $100,000, on a hypothetical capital growth of 10% YoY and $0 cash flow neutrality between its yield and its running costs, after the 25% tax on its sales, only takes… about the 10 same years.

Yet, what is asked of the first person is the kind of life that allows them to be paid $412,000 p.a. for the next 10 years, while the second person “only” needs to come up with $100,000 to begin with, and have the market carry them up.

When the direction is up, compounding becomes your friend, as you compound over $1,000,000 instead of your actual $100,000.

Inflation becomes your friend, as the 4% yearly erosion of your money-now makes your debt cheaper each year.

The tax treatment becomes your friend, as long as the powers that be keeps taxing capital growth less than it does earned income.

All of these can be had, at the cost of not being able to use it now.

One can never eat capital growth. It is only after a “liquidity event”, the alchemy with which paper turns into currency, that this becomes a liquid capital — usually money — to use.

When one sells, one forfeits the right for the future possible gains (and losses), as the asset ceases to be one’s own.

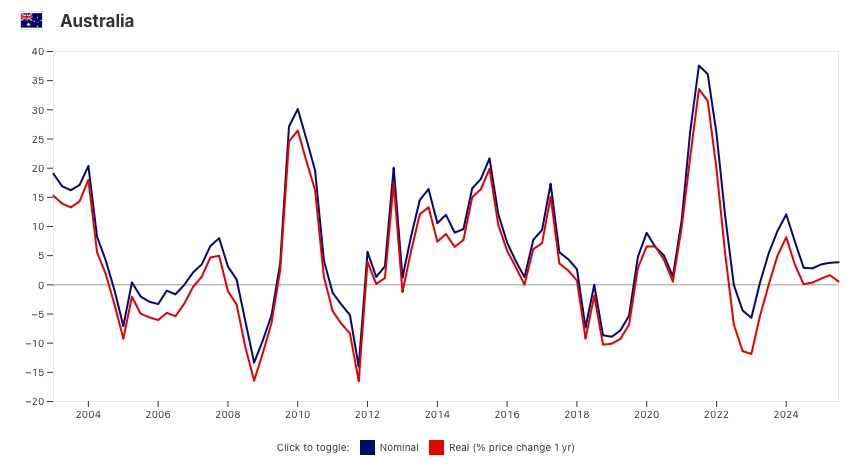

In the face of the average expected yields…

…and expected average capital growths…

…and a lender’s limitations on how much to lend…

…we, like most people, implicitly accepts the ceiling to an asset’s total possible returns, and bargain with the years instead.

If you have never seen a balance sheet before, learn it.

In this game of wealth, accounting is score-keeping, in the form of your net worth. You won’t know how to improve if you have no sense of how things are currently going.

What a net worth is not, is your self worth.

The expense tracking in A Tale of Three Brackets: Part 1 is one half of the standard Financial Statements: Cash Flow Statement, which deals with the matters of money now.

Balance Sheet deals with money past. It is a snapshot of your total assets at a particular slice in time, which is useful to track the overall direction one is moving, but is useless when it comes to the day-to-day, as having one’s eyes fixated on the written stars above means that one is at risk of stepping on loose stones below.

And yet… enough is not found in-between the steps, but in the appreciation that comes into view when one stops, looks around, and realise how far you’ve come.

Financial Projections, on the other hand, is not a financial statement.

There is a simple reason why financial projections don’t count as a financial statement: it’s not based on any fact.

For something to be factual, it has to have happened. If it hasn’t happened yet, how can it be true? This goes for any investment thesis and projections, no matter how “sure-bet” it is. In this sense all projectors and dreamers are liars, for the things they tell can never be true at the time of telling.

Yet there may come a time when it comes true, and so one hedges for the worst, and invest for the best.

Start with one set of financial statement: your personal balance sheet and cash flow statement.

The rest is about learning how to accumulate faster... without losing sight of what truly matters.

If one wants to learn the game of wealth creation, one must learn how to see things as they are. This is wealth preservation 101.

At the same time, one, too, must learn how to see things as they could be, in order to create the reality that one wants. This is wealth creation 101.

The language is contracts, and it speaks in %s of proportions and probabilities.

Enough money, in the context of growing wealth, is enough seeds to sow, or more commonly referred to as “ticket to play”.

With enough money to afford losses, one can now afford taking chances.

The more tickets one has, the more chances one can take.

The more one can risk, the more one can potentially gain, though a return is never guaranteed no matter how many people try to convince you that they’ve found “the secret to riches”. This is why putting all of one’s eggs in one basket is the strategy of the desperate: the ones who have nothing to lose, and the ones who have no other way than to make it work.

For everyone else, the long game is the sane game: risk some to win some, and still afford life in its entirety. Why aim for a good life if one doesn’t take time and enjoy that bit?

…this lukewarm point is where most people get stuck at.